- PE 150

- Posts

- Family Office Private Equity Surge: $9.5T by 2030

Family Office Private Equity Surge: $9.5T by 2030

Family Offices are becoming key LPs in private equity. Global wealth set to reach $9.5T by 2030, with 45% allocation to alternative assets.

In this article

Market Overview

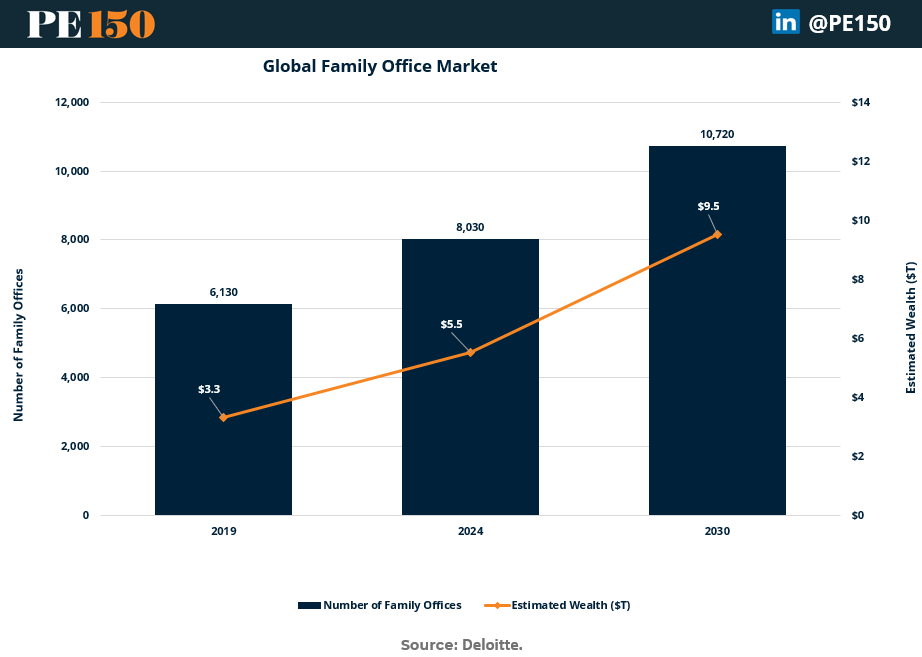

The Family Office private equity investment market continues to expand at a robust pace, solidifying its role as a significant force in global wealth management. According to Deloitte, the number of Family Offices worldwide is projected to surpass 8,000 in 2024, representing a total estimated wealth of approximately $5.5 trillion. This marks a substantial 31% increase over the 6,130 Family Offices recorded in 2019.

More notably, total wealth managed by Family Offices has grown by 66.7% over the same five-year period, indicating not only an increase in their number but also a trend toward managing larger pools of capital.

Looking ahead, the Family Office market is expected to experience continued momentum. By 2030, the number of Family Offices is forecasted to exceed 10,000, reflecting a 33.5% growth from 2024, with the total wealth managed projected to reach $9.5 trillion—a 72.7% increase compared to 2024. This sustained growth highlights the rising influence and capacity of Family Offices to manage significant and growing levels of wealth globally.

According to Deloitte, Family Offices are not only growing in number but also expanding across regions. In 2024, North America will dominate the global Family Office landscape, accounting for approximately 39% of the total, followed by Europe at 25% and Asia Pacific at 28%. The remaining share is distributed among the Middle East (4%), South America (2%), and Africa (1%).

Looking at the evolution, North America is expected to experience steady growth, increasing from 3,180 Family Offices in 2024 to 4,190 by 2030. Similarly, Europe and Asia Pacific will see significant increases, reaching 2,650 and 3,200 Family Offices respectively by 2030. While smaller in absolute numbers, regions like the Middle East, South America, and Africa will also show steady growth. The global total is projected to surpass 10,000 Family Offices by 2030, reinforcing the expanding influence of Family Offices worldwide and their increasing role in wealth management across diverse geographies.

Family Offices Asset Allocation and Investment Strategies

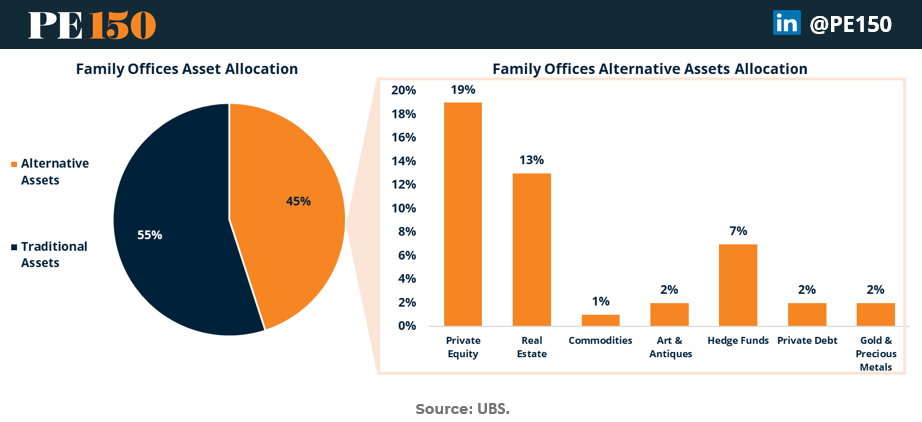

According to a recent study conducted by UBS, Family Offices allocate approximately 55% of their portfolios to Traditional Assets (such as public equities, bonds, and cash) and 45% to Alternative Assets, demonstrating a balanced yet strategically diversified approach to wealth management.

Within the Alternative Assets category, Private Equity emerges as the most dominant asset class, accounting for 19% of total investments. This is closely followed by Real Estate, which represents 13% of the portfolio. The prominence of these asset classes aligns with the core investment philosophy of Family Offices, which prioritizes long-term capital preservation and steady returns over short-term volatility.

Private Equity resonates with Family Offices due to its potential for high returns through strategic, long-term investments in private companies and innovative sectors. Real Estate remains equally attractive because of its ability to generate stable income, preserve wealth, and hedge against inflation over extended time horizons. These preferences reflect the fundamental approach of Family Offices—favoring patient capital that supports sustainable growth and generational wealth transfer, while reducing exposure to the volatility associated with public markets.

The growing allocation to Alternative Assets also highlights the increasing sophistication of Family Offices as investors. Their ability to take on illiquidity risks, conduct thorough due diligence, and directly access private market opportunities has positioned them as key players in Private Equity and Real Estate markets globally. For Private Equity investors, this represents a significant opportunity to collaborate with Family Offices, leveraging their long-term focus, capital stability, and appetite for transformative investments.

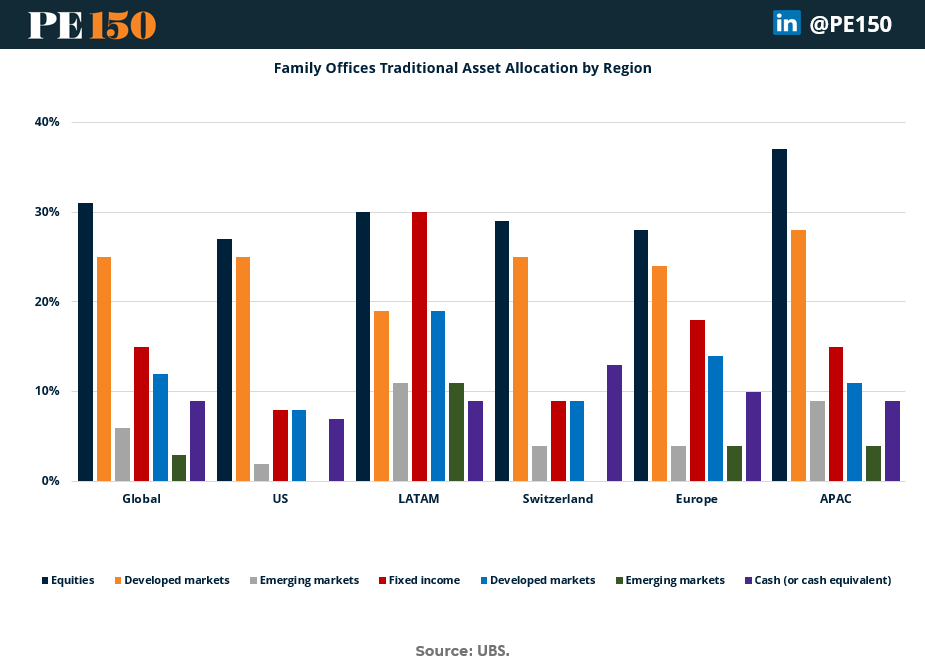

According to UBS, Family Offices demonstrate a well-diversified investment strategy, balancing Traditional and Alternative assets across regions to achieve sustainable growth and wealth preservation. On a global scale, Family Offices allocate approximately 31% of their portfolios to equities, followed by 25% to developed market fixed income and 15% to emerging markets and bonds. This reflects a continued reliance on Traditional Assets to provide stability while maintaining exposure to public market opportunities.

Regionally, APAC leads the allocation in equities with 37%, reflecting its strong growth markets and investor confidence. In contrast, LATAM exhibits the highest allocation to fixed income at 30%, prioritizing stability in more volatile market conditions. The US remains focused on developed markets (25%), while Switzerland and Europe display a balanced allocation across traditional assets, signaling a preference for diversification.

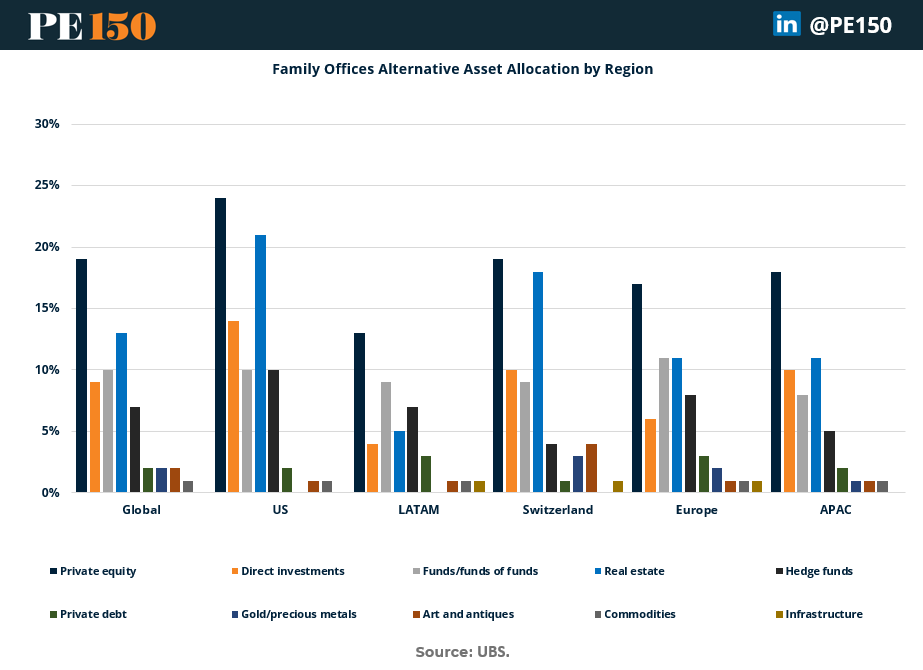

On the Alternative Assets front, Private Equity continues to dominate globally, with an average allocation of 19%, underscoring Family Offices' appetite for high returns and long-term capital appreciation. Real Estate follows at 13%, given its role in providing stable income and hedging inflation. Notably, the US has the largest allocation to Private Equity at 24%, driven by its strong ecosystem of private markets and deal flow opportunities. In contrast, Switzerland and Europe show significant investments in Real Estate at 18% and 11%, respectively.

Other key Alternative Assets include Direct Investments (10%) and Hedge Funds (7%), particularly in regions like the US and LATAM, where Family Offices demonstrate a growing appetite for more direct, active management strategies. Allocations to Private Debt and Gold/Precious Metals, while smaller globally, highlight the ongoing efforts to diversify portfolios and hedge against market uncertainty.

In summary, UBS data reveals that Family Offices are increasingly blending Traditional and Alternative investments, with Private Equity and Real Estate emerging as core pillars of long-term investment strategies. The regional variations further illustrate the adaptive nature of Family Offices, responding to local opportunities and economic environments while maintaining their focus on capital preservation and growth.

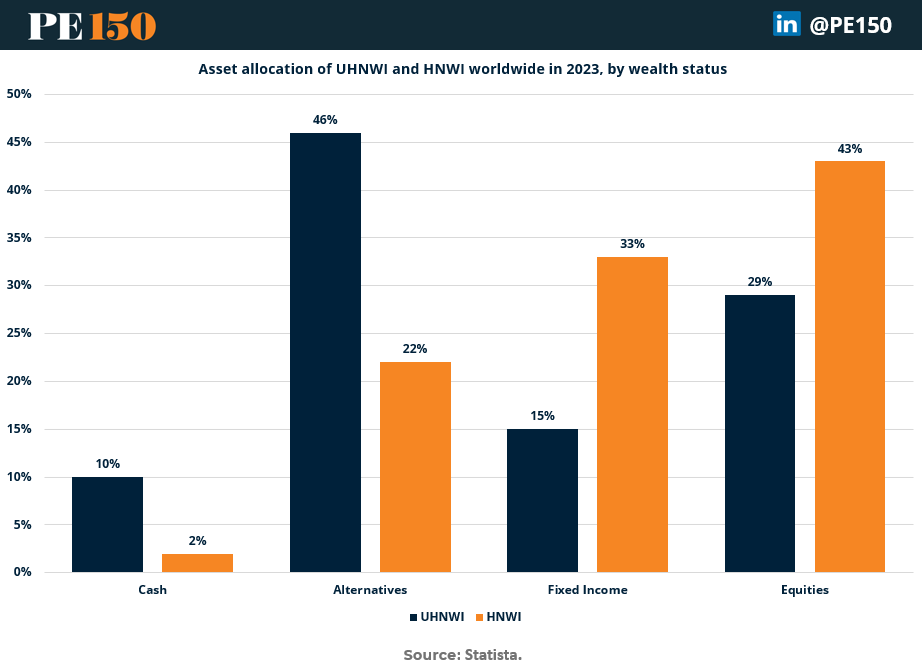

According to Statista, the asset allocation of Ultra High Net Worth Individuals (UHNWIs) and High Net Worth Individuals (HNWIs) in 2023 highlights key differences in their investment strategies. UHNWIs allocate a significant 46% of their portfolios to Alternatives, showcasing their preference for long-term, higher-yielding investments such as Private Equity, Real Estate, and other non-traditional asset classes. In comparison, HNWIs allocate only 22% to Alternatives, prioritizing liquidity and shorter investment horizons.

Equities also play a prominent role, with HNWIs allocating 43% to this asset class compared to 29% for UHNWIs, indicating a stronger focus on public market opportunities among HNWIs. In contrast, UHNWIs maintain 10% in Cash, a notably higher proportion compared to 2% for HNWIs, reflecting UHNWIs’ strategic flexibility to seize investment opportunities.

Lastly, Fixed Income comprises 33% of HNWI portfolios versus 15% for UHNWIs, signaling HNWIs' preference for lower-risk, income-generating assets. These findings underscore how UHNWIs prioritize Alternative Investments and diversification for capital growth, while HNWIs lean toward Equities and Fixed Income for stability and returns in a more liquid environment.

Most Attractive Investment Themes for Family Offices

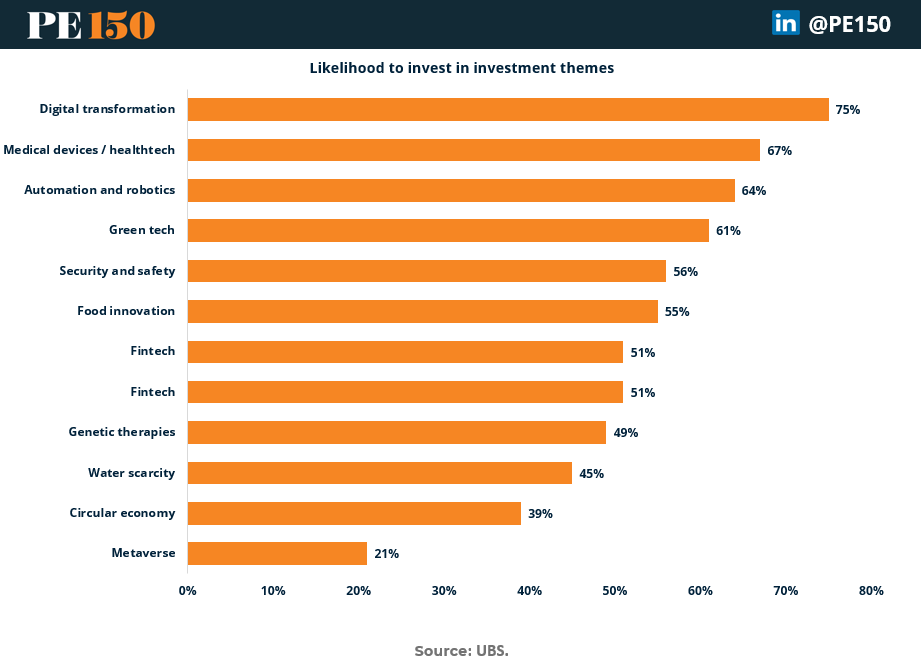

According to UBS, Family Offices demonstrate a strong focus on innovative and high-growth sectors when it comes to future investment themes. Topping the list is Digital Transformation, with 75% of Family Offices showing a likelihood to invest in this area, underscoring the increasing importance of technology-driven business models and digital infrastructure in shaping global markets.

Medical Devices and HealthTech follows closely, attracting interest from 67% of Family Offices. This reflects growing opportunities in healthcare innovation, driven by advancements in medical technology and a rising demand for solutions that enhance patient care and longevity. Similarly, Automation and Robotics (64%) and Green Tech (61%) rank highly, showcasing a strong appetite for investments in efficiency, sustainability, and emerging technologies that address critical global challenges.

Investment in Security and Safety (56%) and Food Innovation (55%) highlights a focus on industries that address fundamental societal needs, such as cyber security, physical protection, and sustainable food systems. Meanwhile, Fintech remains a key theme at 51%, reflecting confidence in the transformation of financial services through technology.

Emerging sectors like Genetic Therapies (49%), Water Scarcity Solutions (45%), and the Circular Economy (39%) also reflect growing interest in investments that align with long-term societal and environmental impact. However, Metaverse lags behind at 21%, indicating a more cautious approach toward virtual reality and digital asset themes among Family Offices.

Overall, these investment priorities reveal that Family Offices are targeting sectors with significant growth potential, technological innovation, and sustainability focus, reflecting a blend of long-term value creation and alignment with global megatrends.

Last Year Private Equity Investments by Family Offices

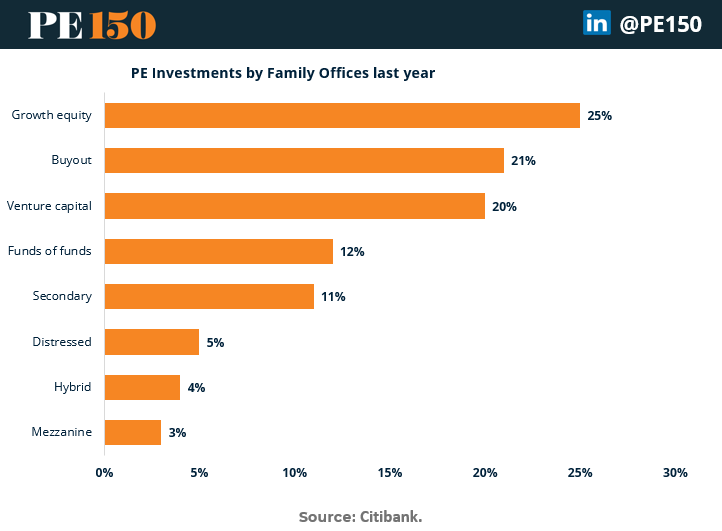

According to Citibank, Private Equity (PE) investments made by Family Offices last year were concentrated in a mix of growth-oriented and strategic opportunities, reflecting their long-term investment approach and focus on value creation. Growth Equity led the way, accounting for 25% of PE investments, as Family Offices sought opportunities to scale businesses with proven models and strong growth potential.

Buyouts followed closely at 21%, underscoring the appetite for controlling stakes and strategic acquisitions to enhance operational efficiencies and profitability. Similarly, Venture Capital represented 20% of PE investments, highlighting a willingness to invest in innovative startups and early-stage companies with high return potential.

Other notable categories included Funds of Funds (12%) and Secondary Investments (11%), indicating a preference for diversified exposure to private markets and liquidity solutions. Meanwhile, smaller allocations were made to specialized segments like Distressed Assets (5%), Hybrid Strategies (4%), and Mezzanine Financing (3%), which cater to more niche opportunities in the private equity landscape.

This distribution reflects Family Offices' growing sophistication and ability to engage across various PE strategies. Their focus on Growth Equity and Venture Capital aligns with their long-term philosophy, while participation in Buyouts and Secondaries suggests a diversified approach to managing risk and seizing strategic opportunities in private markets.

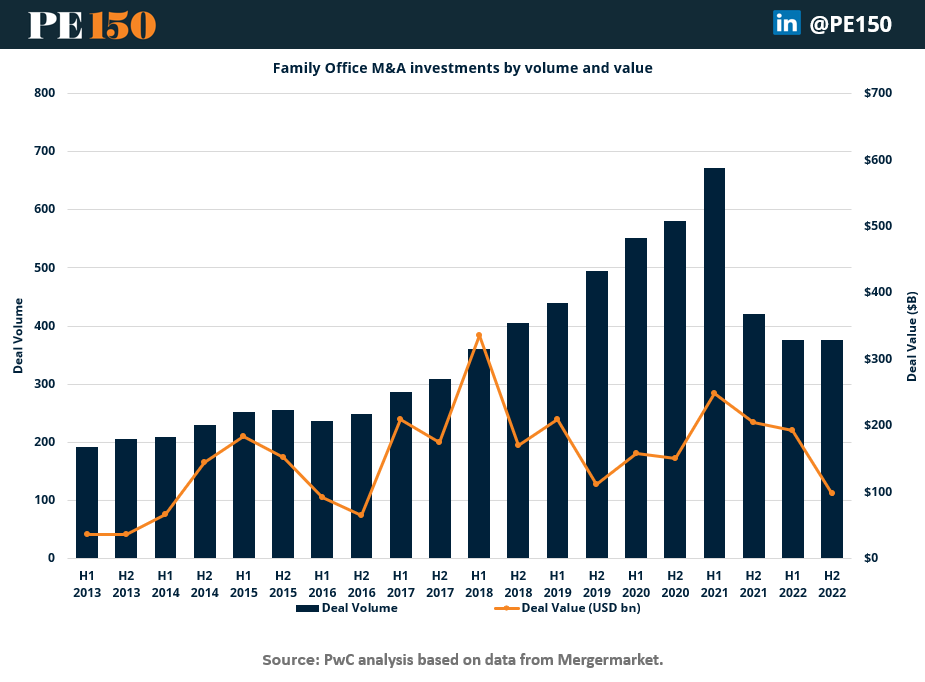

Family Office investments by volume and value

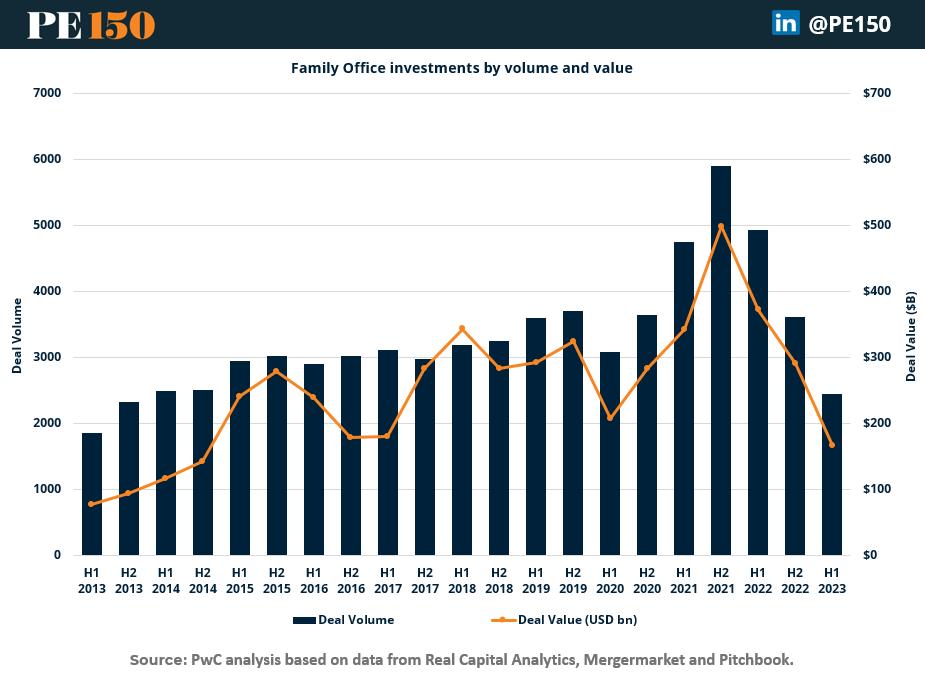

According to the 2023 Family Office Market study conducted by PwC, global Family Office investment volume and value have experienced a significant decline following their peak in 2021. Over a 3-year period, from the first half of 2021 (1H21) to the first half of 2023 (1H23), the investment activity registered a notable decrease of approximately 51%. This contraction reflects the challenges posed by global economic uncertainty, rising interest rates, and shifting market dynamics, which have collectively led to more cautious investment strategies among Family Offices. Despite this decline, Family Offices remain resilient and adaptable, prioritizing selective opportunities and long-term capital preservation strategies amid a changing macroeconomic landscape.

In line with this trend, Family Offices' M&A investments have also experienced a significant decline following a bullish 2021, which marked a record-breaking period for deal activity. During the first half of 2021 (1H21) alone, M&A investments reached an impressive value of over $247 billion, showcasing the heightened appetite for strategic acquisitions and growth opportunities during that time. However, this momentum has since slowed considerably, reflecting the impact of economic headwinds, increased valuation scrutiny, and a more cautious investment environment. Despite the downturn, Family Offices continue to remain key players in the M&A space, selectively pursuing high-quality opportunities aligned with their long-term investment objectives.

Geographic Analysis for Family Office Business

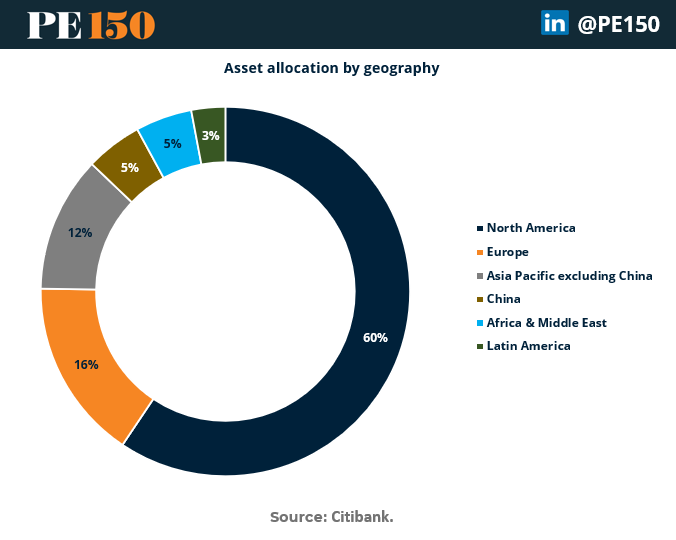

Family Office Asset Allocation by Region

Family office asset allocation shows a strong preference for North America, which holds 60% of the investments. Europe follows with 16%, while the Asia Pacific excluding China accounts for 12%. Smaller allocations include China at 5%, Africa & Middle East at 5%, and Latin America with 3%. This highlights a significant concentration of investments in developed markets, particularly North America, with limited exposure to emerging regions.

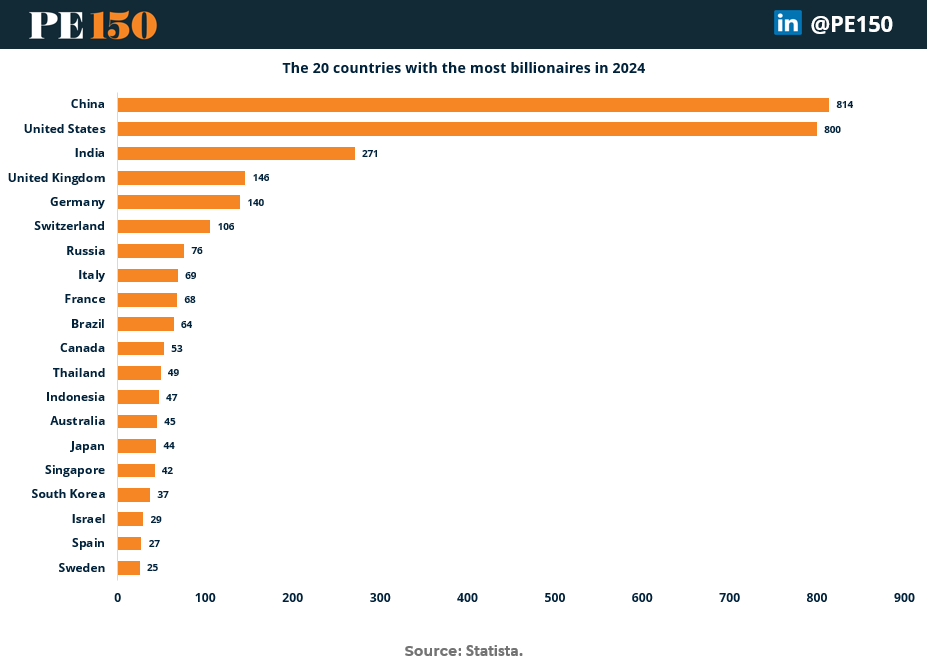

The 20 countries with the most billionaires in 2024

According to Statista, China and the United States lead the world with the highest number of billionaires in 2024, boasting 814 and 800 billionaires, respectively. India follows in third place with 271, while other key countries like the United Kingdom (146), Germany (140), and Switzerland (106) round out the top positions. This concentration of ultra-wealthy individuals is significant for the Family Office business, as it highlights regions with the greatest demand for wealth management, succession planning, and investment services. The increasing number of billionaires, particularly in emerging economies like India and growing markets across Asia, represents a robust opportunity for Family Offices to offer tailored solutions, including alternative investments, private equity, and philanthropy strategies. This trend underscores the growing importance of Family Offices as essential partners in preserving and expanding generational wealth in an increasingly complex global landscape.

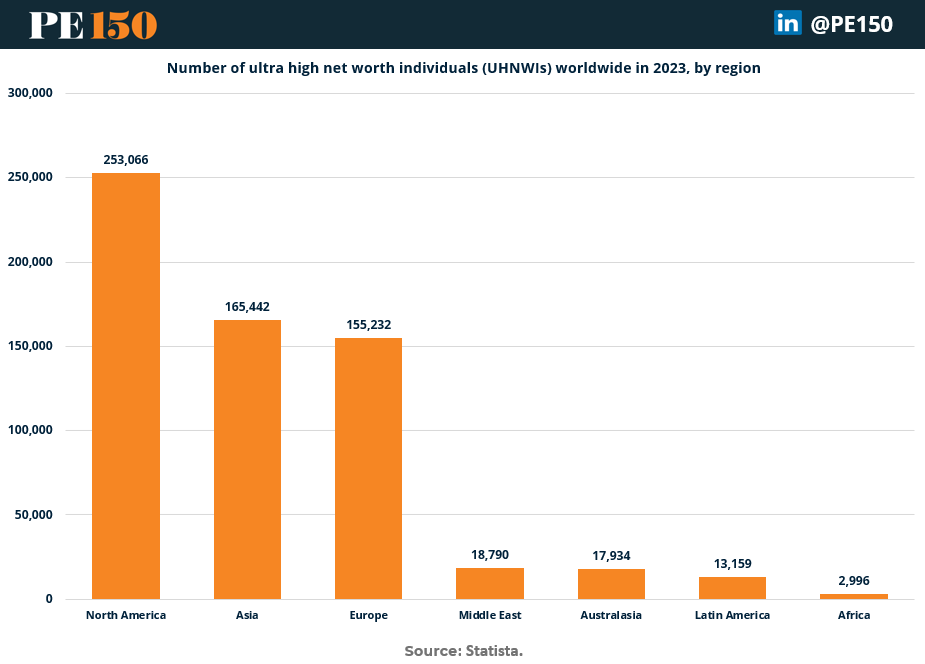

Number of ultra-high net worth individuals (UHNWIs) worldwide in 2023, by region

North America leads the world in the number of Ultra High Net Worth Individuals (UHNWIs) in 2023, with 253,066 individuals, followed by Asia (165,442) and Europe (155,232). Other regions, such as the Middle East (18,790), Australasia (17,934), Latin America (13,159), and Africa (2,996), also contribute to the global UHNWI population, albeit on a smaller scale.

This geographic distribution is significant for the Family Office industry, as North America, Asia, and Europe remain key markets for wealth management, estate planning, and investment services. The growing concentration of UHNWIs in Asia highlights the region’s rising economic power and underscores opportunities for Family Offices to provide tailored solutions, particularly in emerging economies. Additionally, the presence of wealth in regions like the Middle East and Latin America signals potential for expansion in wealth preservation strategies and investment diversification. As UHNWIs seek to preserve and grow generational wealth, Family Offices will play a critical role in delivering personalized, long-term financial and strategic solutions across these global markets.

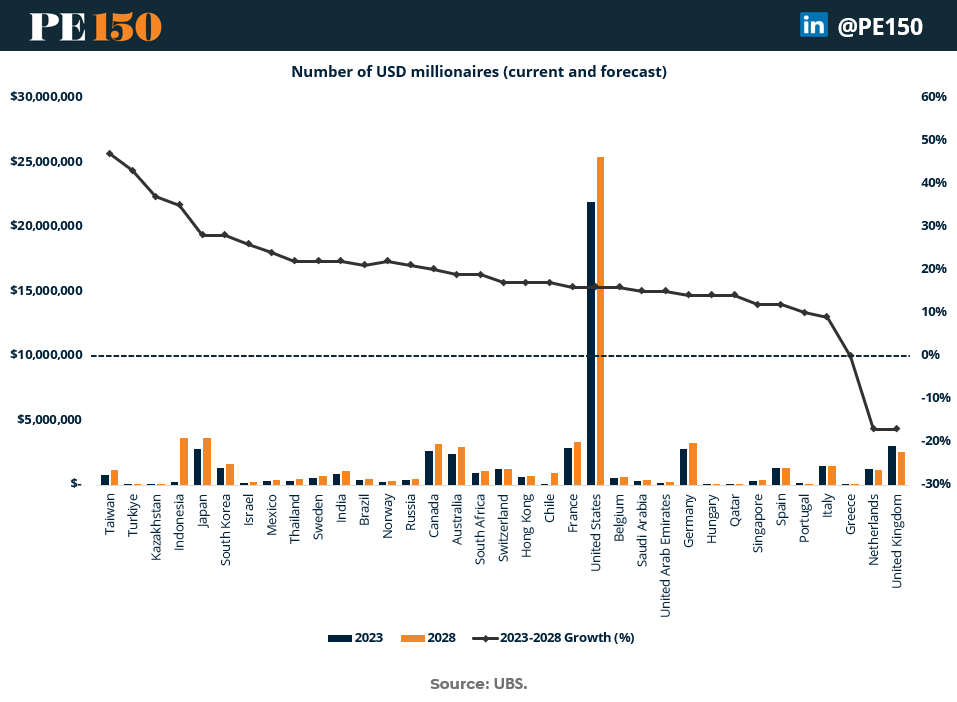

Top Countries by number of USD millionaires and 2028E Forecast

According to the Global Wealth Report by UBS, the number of USD millionaires is projected to grow significantly in many countries between 2023 and 2028, reflecting shifting global wealth dynamics. Taiwan leads the way with a remarkable 47% growth, increasing its millionaire population from 788,799 in 2023 to 1,158,239 by 2028. Türkiye and Kazakhstan follow closely, with projected growth rates of 43% and 37%, respectively, highlighting the rapid economic development in emerging markets.

In Asia, Indonesia stands out with a notable 35% increase, while advanced economies like Japan and South Korea are expected to grow by 28% each, showcasing sustained economic expansion in the region. Similarly, Mexico and India are forecast to grow their millionaire populations by 26% and 22%, reflecting robust economic activity and wealth accumulation.

Meanwhile, Canada and Australia will see more modest gains of 20% and 19%, respectively, while Switzerland, Chile, and Russia show steady increases of around 17%. In contrast, countries like the Netherlands and the United Kingdom are expected to experience negative growth, with declines of -17%, signaling potential economic challenges or wealth shifts in these regions.

This growth in millionaire populations, particularly in emerging markets like Asia and parts of Latin America, represents significant opportunities for Family Offices and wealth managers. As wealth creation accelerates, the demand for services such as investment advisory, estate planning, and alternative investments will continue to rise. Family Offices can play a critical role in helping these newly affluent individuals preserve and grow their wealth across generations, particularly in rapidly evolving economic landscapes.

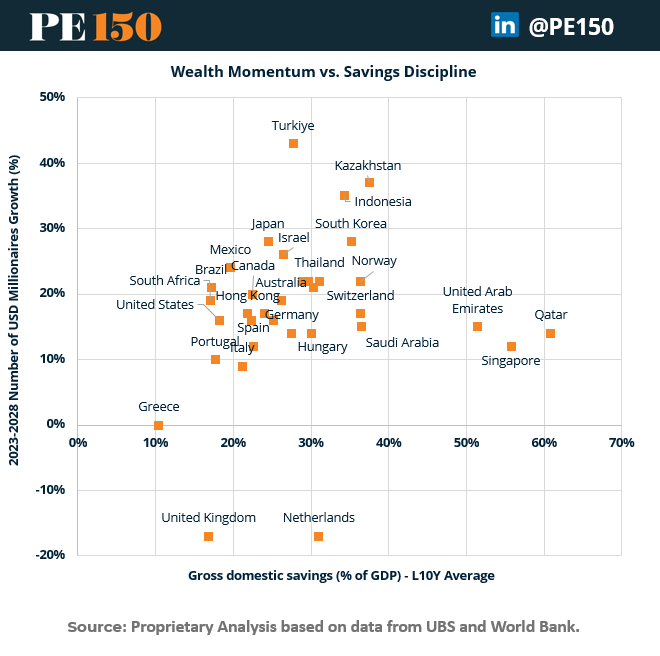

Proprietary Analysis: Wealth Momentum vs. Savings Discipline

This scatter plot illustrates the relationship between Wealth Momentum—measured as the projected 2023–2028 growth in the number of USD millionaires (%)—and Savings Discipline, represented by the Gross Domestic Savings (as a % of GDP, 10-year average) across various countries.

Key Insights:

Top-Right Quadrant (High Savings, High Growth):

Countries like Kazakhstan, Indonesia, South Korea, and Türkiye exhibit both strong gross domestic savings and high projected millionaire growth. This combination reflects disciplined savings habits and rapid economic development, creating a conducive environment for wealth accumulation. For Family Offices, these markets present significant opportunities to serve newly affluent individuals seeking wealth management and investment strategies to preserve and grow their capital.

Top-Left Quadrant (Low Savings, High Growth):

Countries like Japan, Mexico, and Brazil show robust millionaire growth despite relatively lower gross savings rates. This indicates that wealth creation in these regions is being driven by factors like business success, innovation, and investment inflows rather than household savings alone. Family Offices can target these regions with tailored solutions, particularly in areas like succession planning, private equity, and diversified investments to support sustainable wealth growth.

Bottom-Right Quadrant (High Savings, Low Growth):

Countries such as Singapore, Qatar, and Saudi Arabia have high savings rates but slower projected millionaire growth. While wealth accumulation may be steady, Family Offices can add value by helping affluent individuals optimize their existing wealth through more sophisticated investment strategies, international diversification, and alternative investments like real estate or private markets.

Bottom-Left Quadrant (Low Savings, Low Growth):

Countries like Greece, the United Kingdom, and the Netherlands face both low savings rates and negative or stagnant millionaire growth. These markets present fewer immediate opportunities but may benefit from Family Offices offering specialized wealth preservation strategies to maintain capital in challenging economic environments.

Why This Matters for Family Offices:

High-Growth Markets: Emerging economies with strong savings discipline, such as Türkiye, Kazakhstan, and Indonesia, represent major opportunities for Family Offices to enter rapidly expanding markets, establish relationships with newly affluent families, and provide expertise in wealth management, asset allocation, and estate planning.

Wealth Optimization: Even in markets with slower millionaire growth but high savings rates, like Singapore and the Middle East, Family Offices can deliver value by helping clients diversify investments and achieve higher returns through alternative assets and international strategies.

Tailored Solutions: Regions like Japan and Mexico, where millionaire growth is robust, but savings are lower, indicate the need for tailored financial solutions to support wealth preservation and intergenerational transfer.

In summary, this scatter plot highlights dynamic opportunities for Family Offices to grow their business globally. By focusing on markets with high wealth momentum and understanding regional economic behaviors, Family Offices can play a pivotal role in helping families manage, protect, and grow their wealth over the long term.

Conclusion

Family office private equity investment are increasingly emerging as key Limited Partners (LPs) in the Private Equity landscape, offering a unique blend of patient capital, long-term focus, and strategic flexibility. With global Family Office wealth projected to reach $5.5 trillion in 2024 and grow by over 72% by 2030, these entities are well-positioned to deepen their engagement in Private Equity. Their preference for Growth Equity, Buyouts, and Venture Capital aligns perfectly with the transformative and high-return opportunities that PE funds provide. To attract Family Offices as LPs, Private Equity firms must emphasize tailored investment opportunities, transparent partnerships, and alignment with Family Offices' core philosophies of capital preservation and long-term value creation. By addressing their increasing sophistication and appetite for alternative assets, Private Equity investors can unlock a resilient and growing source of capital to fuel ambitious and sustainable growth strategies.

Sources & References

Citi. (2024). Global Family Office 2024 Survey Insights. https://www.privatebank.citibank.com/doc/family-office/global-family-office-2024-survey-insights.pdf.coredownload.inline.pdf

Deloitte. (2024). Deloitte Private’s latest report in its Family Office Insights Series. https://www2.deloitte.com/content/dam/Deloitte/dk/Documents/Global%20Deloitte%20Private_Top%2010%20Family%20Office%20Trends%202024.pdf

McKinsey. (2024). Asia-Pacific family office boom: Opportunity knocks. https://www.mckinsey.com/~/media/mckinsey/industries/financial%20services/our%20insights/asia%20pacifics%20family%20office%20boom%20opportunity%20knocks/asia-pacifics-family-office-boom-opportunity-knocks.pdf?shouldIndex=false

PwC. (2023). PwC`s Global Family Office Deals Study 2023. https://www.pwc.ch/de/publications/2023/family-office-deals-study-2023.pdf

Statista. (2024). The 20 countries with the most billionaires in 2024. https://www.statista.com/statistics/299513/billionaires-top-countries/

Statista. (2024). Number of ultra-high net worth individuals (UHNWIs) worldwide in 2023, by region. https://www.statista.com/statistics/204072/distribution-of-ultra-high-net-worth-individuals-by-world-region/

Statista. (2023). Asset allocation of ultra and high net worth individuals worldwide in 2023, by wealth status. https://www.statista.com/statistics/1071535/hnwi-asset-allocation-worldwide/#:~:text=Equities%20accounted%20for%20the%20largest,percent%20of%20HNWIs'%20asset%20allocation

UBS. (2023). Global Family Office Report. https://www.ubs.com/content/dam/assets/wm/static/noindex/gfo/docs/ubs-gfo-report-2023.pdf

UBS. (2024). Global Wealth Report. https://www.ubs.com/content/dam/assets/wm/static/noindex/wm-germany/2024/doodownload/Global-Wealth-Report-2024.pdf

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|