- PE 150

- Posts

- The $69 Billion Automation Deal: Private Equity to Back Productivity Growth

The $69 Billion Automation Deal: Private Equity to Back Productivity Growth

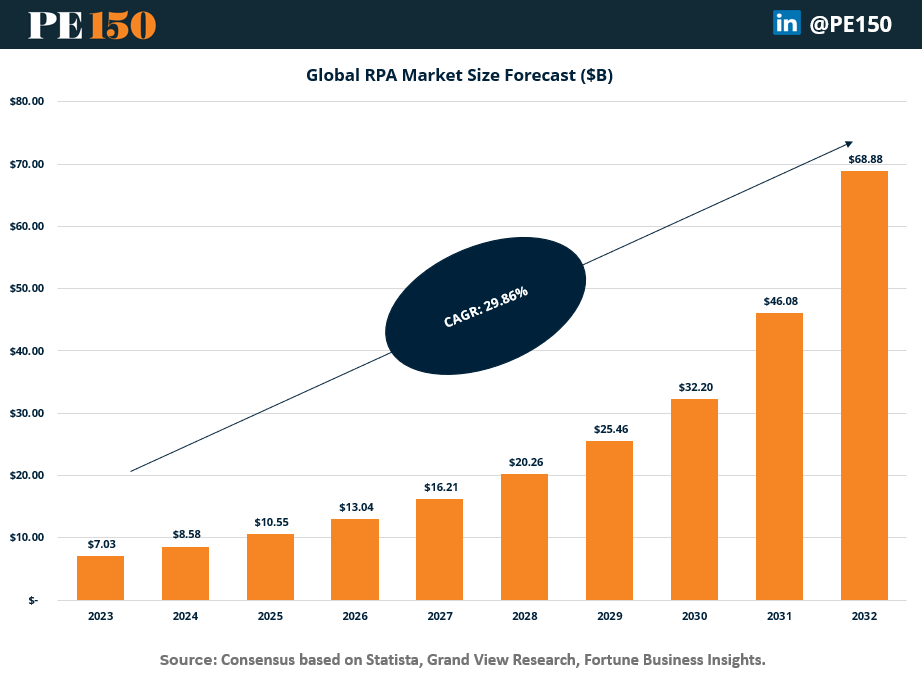

The global Robot Process Automation Market was valued at ~$7 billion in 2023 and it is expected to reach a Total Market Value of ~$68.88 billion by 2032, growing at a CAGR of ~29.86%, driven by increasing demand for automation across various industries to enhance operational efficiency and reduce human error.

In this article

Market Size

Global Robot Process Automation Market was valued at ~$7 billion in 2023 and it is expected to reach a Total Market Value of ~$68.88 billion by 2032, growing at a CAGR of ~29.86%, driven by increasing demand for automation across various industries to enhance operational efficiency and reduce human error.

Main Drivers for RPA Adoption

Cost Efficiency and Operational Savings: Organizations adopt RPA to reduce operational costs by automating repetitive and labor-intensive tasks, allowing businesses to save on human labor and operational inefficiencies.

Enhanced Productivity and Speed: RPA can perform tasks significantly faster than humans, enabling organizations to increase productivity and scale operations without a proportional increase in headcount.

Improved Accuracy and Reduction in Errors: Automating repetitive tasks reduces the likelihood of human errors, ensuring higher accuracy and consistency in data management, reporting, and other critical operations.

Demand for Scalable Solutions: As businesses grow, RPA offers a flexible and scalable solution that can handle increasing workloads without the need for proportional investment in workforce expansion.

Compliance and Risk Management: RPA ensures consistent execution of processes, helping organizations meet regulatory compliance requirements while minimizing risks associated with human intervention, such as data breaches or non-compliance errors.

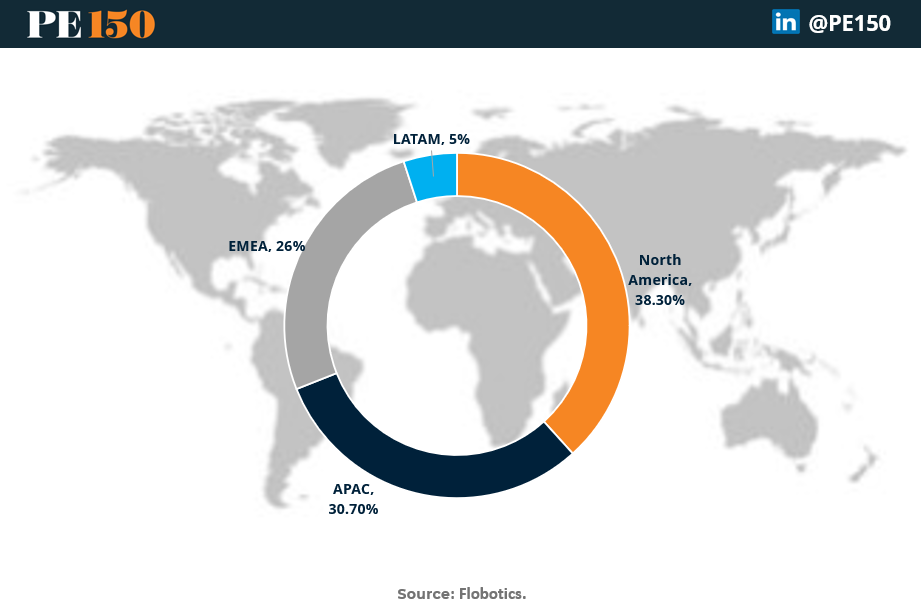

The RPA market share by region highlights the dominance of North America, accounting for 38.30% of the market, driven by the early adoption of RPA technologies, the presence of leading tech companies, and strong investment in automation. The APAC region, with 30.70%, follows as a rapidly growing market due to increased digital transformation efforts, a growing technology and innovation environment, and government initiatives promoting smart manufacturing. EMEA holds 26%, reflecting steady growth attributed to strong adoption in sectors like manufacturing and financial services, alongside compliance-driven demand for automation. Lastly, LATAM represents a smaller share of 5%.

North America RPA Market

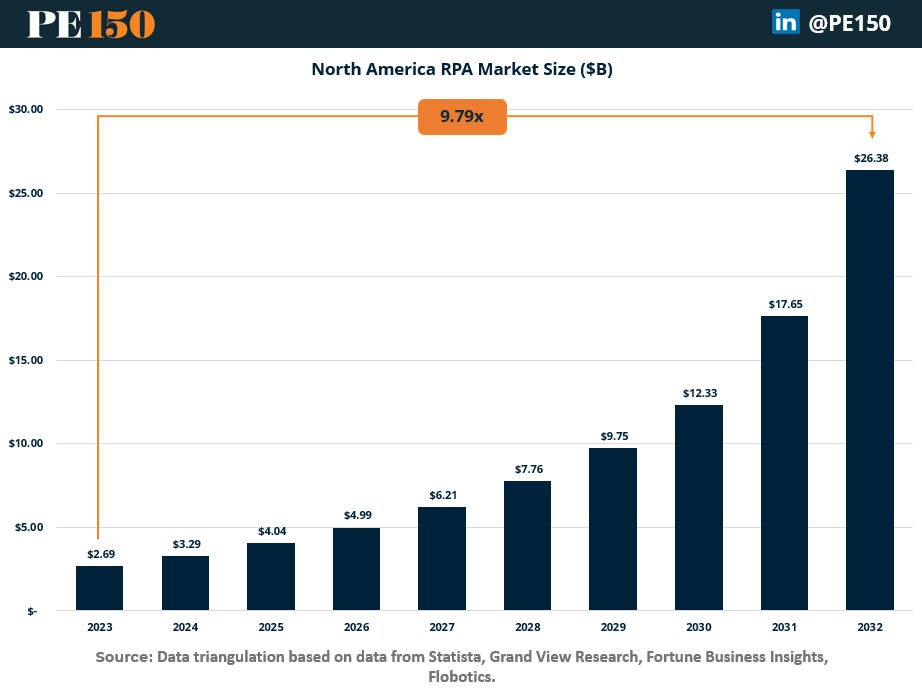

The North America Robotic Process Automation market was valued at ~$2.7 billion in 2023 and it is expected to reach a Total Market Value of ~$26.38 billion by 2032, assuming a constant market share of 38.3%.

North American RPA market is driven by a high level of competition across all industries that pushes to constant innovation and investments in efficiency among companies, to keep competing in a dynamic environment. The US economy is characterized by constant efficiency (output per worker), growth and innovation, pushed by the mentioned high competition it has always had and the world class entrepreneurship environment that keep introducing new players in all markets, year over year.

This landscape presents a significant opportunity for RPA providers to position themselves as critical partners in driving efficiency and innovation for businesses. The growing demand for tailored automation solutions is expected to push the RPA market toward greater fragmentation and specialization. Providers with deep, industry-specific expertise will be better equipped to address the unique challenges and complexities of various sectors, offering customized automation processes that deliver superior efficiency gains. This shift from generalized, one-size-fits-all solutions to highly specialized applications will not only enhance operational outcomes but also redefine the competitive dynamics within the RPA market, fostering a more focused and impactful approach to process automation.

RPA Adoption by Industry

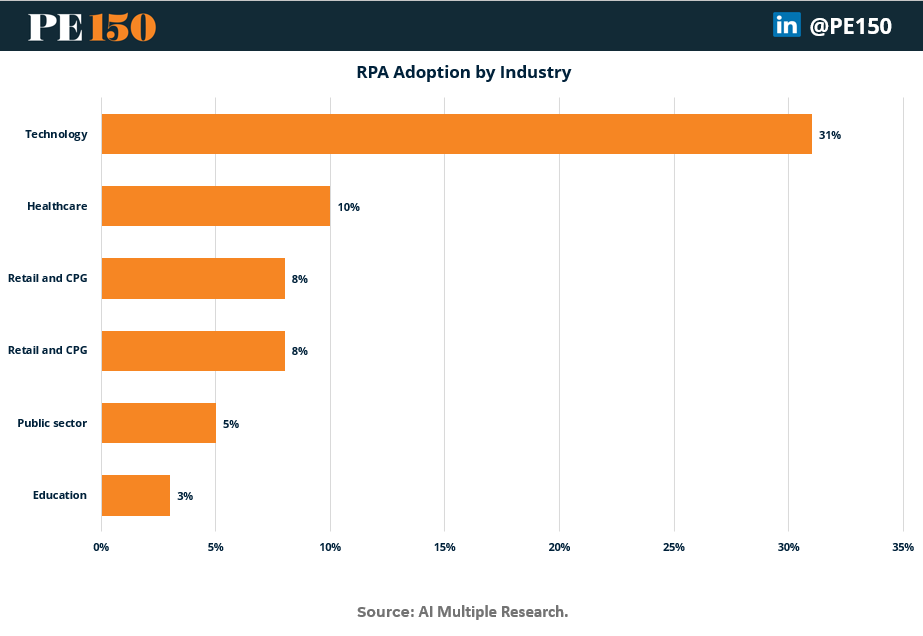

The adoption of Robotic Process Automation (RPA) varies significantly across industries, reflecting the unique needs and priorities of each sector. The Technology sector, with the highest share of 31%, leads in RPA implementation due to its emphasis on innovation, digital transformation, and the automation of complex IT workflows. Healthcare follows with 10%, driven by the need to streamline patient data management, billing processes, and compliance with regulatory requirements. Retail and Consumer Packaged Goods (CPG) account for 8%, leveraging RPA to enhance supply chain operations, customer experience, and inventory management. The Public Sector, at 5%, adopts RPA to improve efficiency in administrative processes and public services. Finally, the Education sector, with 3%, represents the lowest adoption, primarily utilizing RPA for administrative tasks like student enrollment and record management.

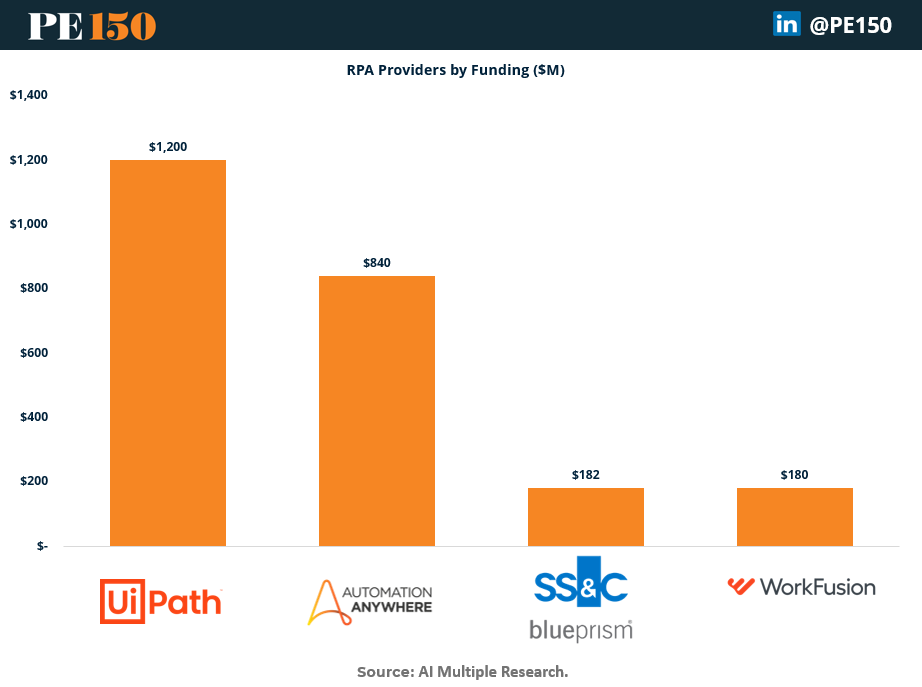

RPA Providers Landscape

According to Gartner Peer Insights, leading Robotic Process Automation (RPA) vendors include UiPath, Automation Anywhere, SS&C Blue Prism, Datamatics, IBM and Microsoft.

The market sees increasing activity from tech giants like IBM and Microsoft, which leverage their extensive ecosystems to integrate RPA into broader automation and cloud solutions. Additionally, newer entrants and niche players are driving innovation, often backed by major corporations or focused on highly specialized industry applications, contributing to a dynamic and competitive landscape.

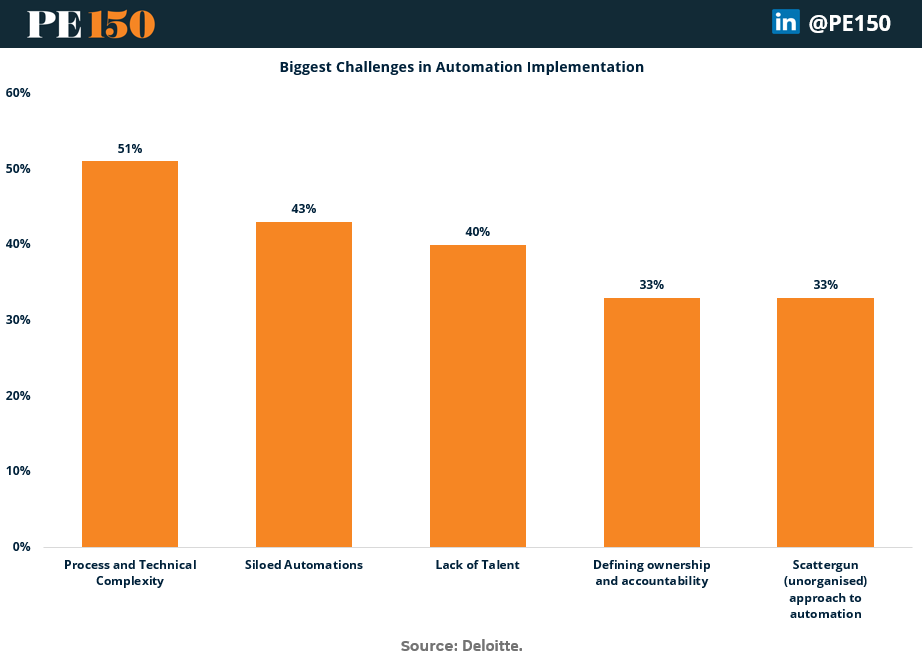

Challenges in Implementation

The Deloitte survey identifies Process and Technical Complexity as the top challenge (51%). Many organizations face difficulties adapting legacy systems, integrating new technologies, and managing complex workflows, delaying automation efforts. A structured approach to process optimization and technological readiness is essential for scaling automation successfully.

Siloed Automations (43%) are a significant hurdle, resulting from isolated departmental efforts that lack alignment with broader organizational goals. While localized benefits may occur, fragmented processes limit scalability and enterprise-wide impact. A centralized governance model and cross-functional collaboration are critical to addressing this challenge.

A Lack of Talent (40%) remains a pressing issue, as the demand for skilled professionals in automation design and deployment outpaces supply. This talent gap slows implementation and risks poor execution. Organizations must invest in training, build internal expertise, and partner with educational institutions to bridge this gap.

The challenge of Defining Ownership and Accountability (33%) arises from unclear roles and responsibilities in automation projects, leading to delays and inefficiencies. Establishing clear accountability at every stage of the automation lifecycle is essential to ensure successful outcomes and timely issue resolution.

A Scattergun Approach (33%), where companies deploy automation without a clear strategy or prioritization, leads to unorganized efforts and wasted resources. Organizations need a systematic, cohesive roadmap driven by strong leadership and a clear vision to maximize the effectiveness of automation.

Deloitte’s findings emphasize the complexity of implementing automation solutions. To overcome these barriers, organizations must focus on process optimization, talent development, clear accountability, and a strategic, integrated approach. Addressing these challenges will unlock automation’s full potential to drive efficiency, innovation, and competitive advantage.

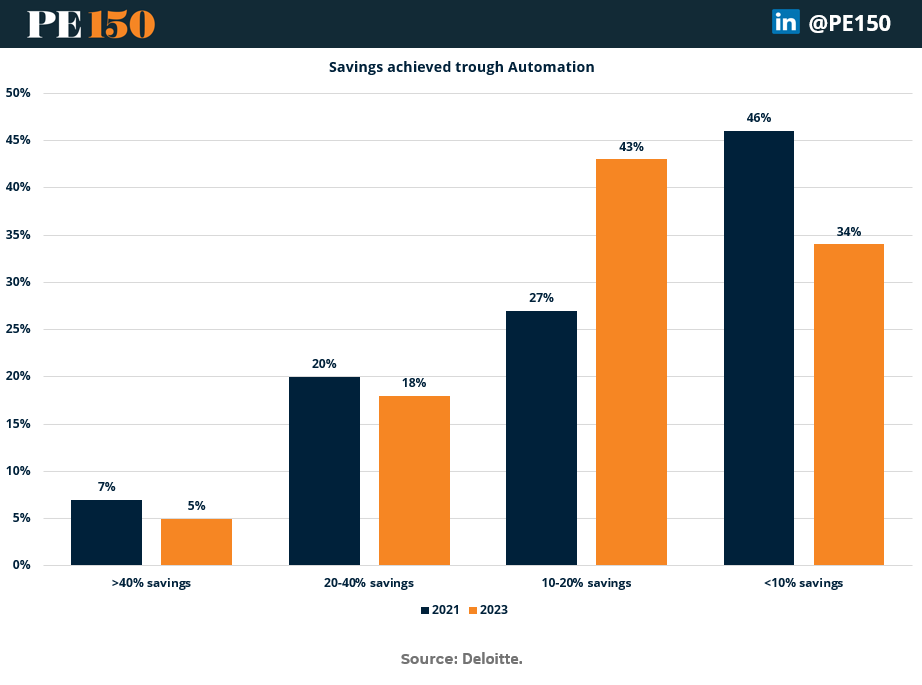

The Deloitte survey shows a shift in automation savings between 2021 and 2023. While the percentage of companies achieving >40% savings dropped from 7% to 5%, those reporting 10-20% savings significantly increased from 27% to 43%, reflecting more moderate but consistent gains. Meanwhile, organizations reporting <10% savings decreased from 46% to 34%, indicating broader improvements in efficiency as automation adoption matures. However, fewer organizations are realizing high-end savings, suggesting opportunities for optimization and better integration of automation strategies.

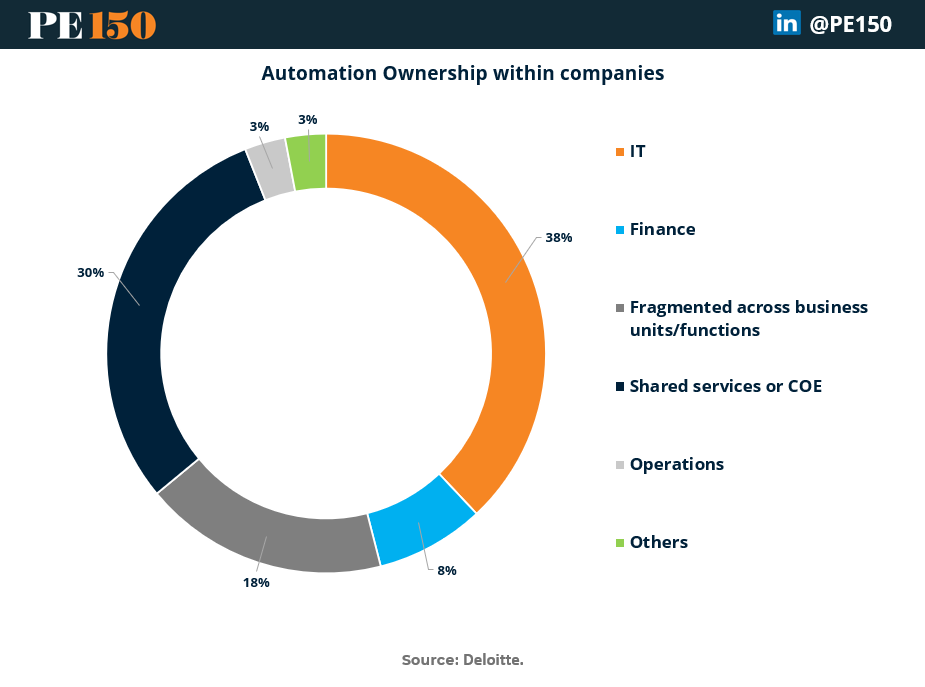

This very insightful survey also highlights the distribution of automation ownership within organizations, revealing distinct patterns. IT departments, at 38%, take the lead in managing automation initiatives, showcasing their critical role in deploying and maintaining technological solutions. Shared Services or Centers of Excellence (COE) follow closely with 30%, indicating a growing preference for centralized governance to ensure scalability and efficiency in automation efforts. However, 18% of organizations report fragmented ownership across business units or functions, which can lead to inefficiencies and a lack of cohesive strategy. Meanwhile, Finance departments account for 8%, reflecting their focused use of automation for tasks like financial reporting and compliance. Operations and Others each represent a small share of 3%, suggesting limited involvement or reliance on centralized automation functions. These findings emphasize the need for clear ownership models to enhance alignment, collaboration, and the overall success of automation strategies.

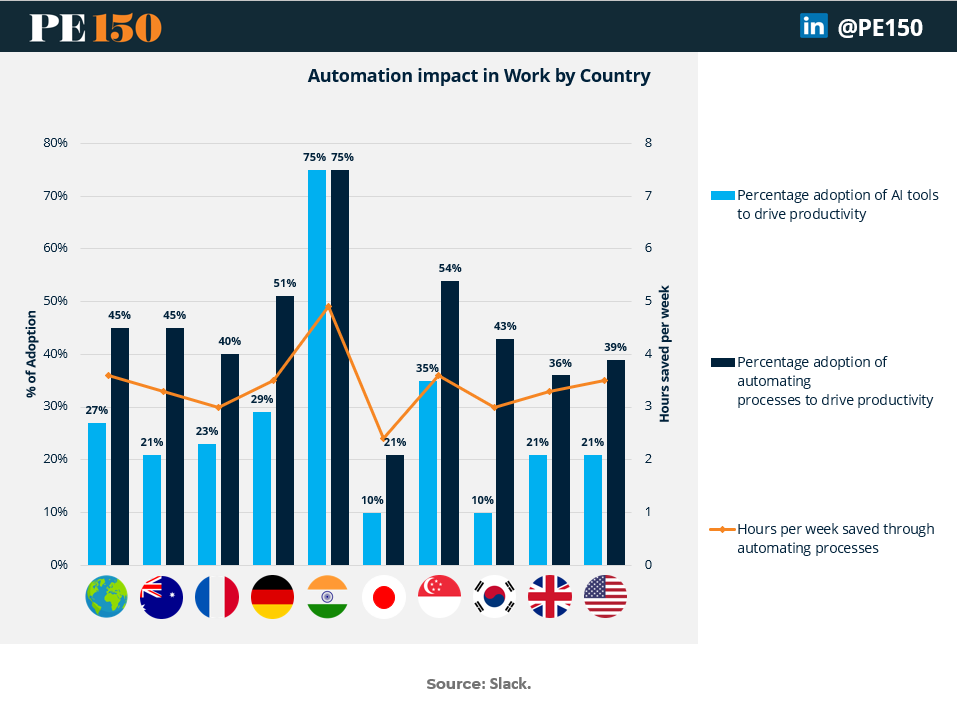

Automation Impact in Work by Country

The 2023 State of Work report by Slack, conducted in partnership with Qualtrics, surveyed 18,149 desk workers and executives across various sectors in nine countries and found that on average, the world saves 3.6 hours per week saved through automating processes, to beat the top barrier to productivity faced by desk workers, like spending too much time in meetings and email.

The report highlights how India is adopting fast AI tools and automation solutions to drive efficiency and labor productivity across many sectors, outperforming world`s average, with an impressive average weekly save of 4.9 hours.

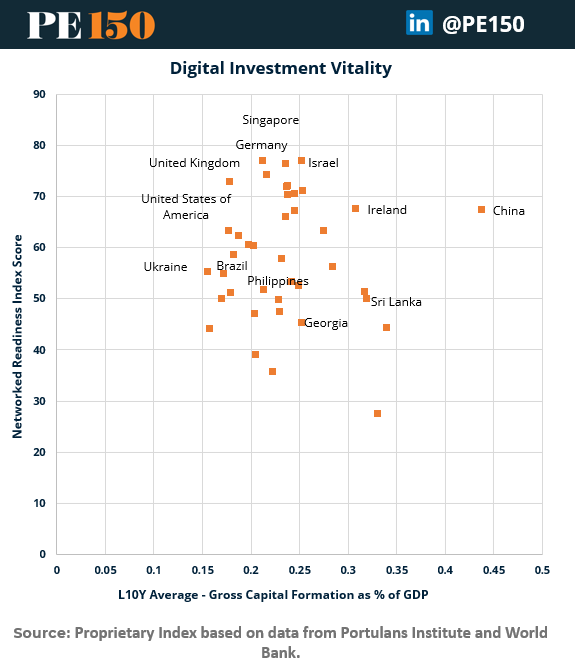

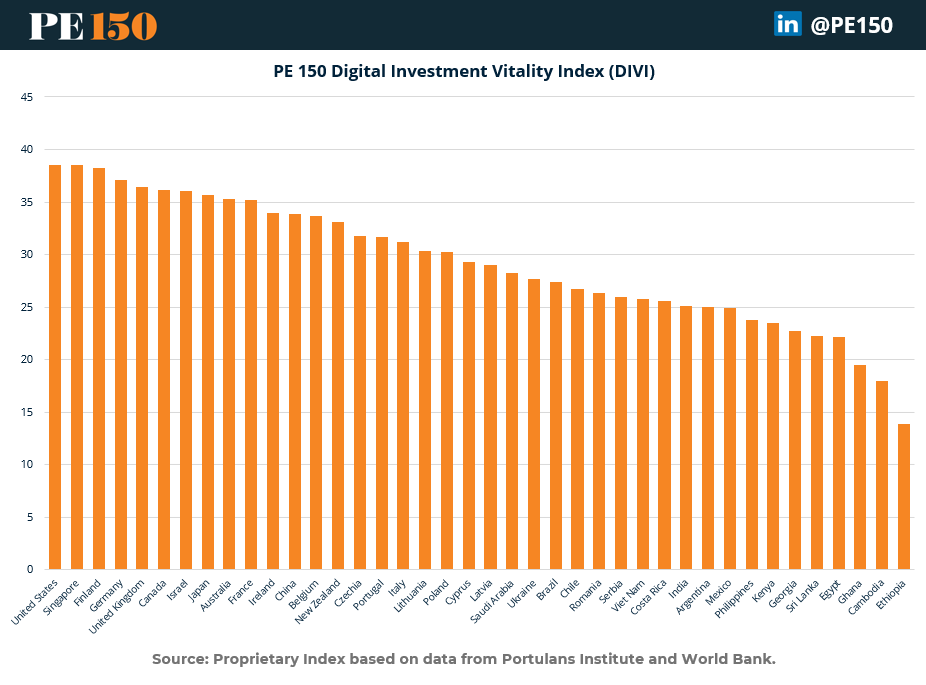

Key Target Markets for RPA and Digital Businesses Growth

Robotic Process Automation market fixes in our Digital Investment Vitality Index analysis, that highlights the key geographic targets for digital innovation segments like RPA.

Our PE 150 Digital Investment Vitality Index (DIVI) balances the Networked Readiness Index Score as a proxy for Technology Infrastructure and L10Y Average - Gross Capital Formation as % of GDP, as a proxy for growth and investment rate, being crucial to understand what the best environments for digital investments are, combining strong technology infrastructures with increasing demand and investments in new solutions.

Conclusion

The global Robotic Process Automation (RPA) market presents a remarkable opportunity for private equity firms to back growth and create value in one of the fastest-growing technology segments. With a projected market size increase from ~$7 billion in 2023 to ~$68.88 billion by 2032, and a robust CAGR of ~29.86%, the sector is ripe for strategic investment. The strong demand for automation, driven by the need for operational efficiency, scalability, and compliance, ensures steady growth across diverse industries, with technology, healthcare, and manufacturing taking the lead.

Geographically, North America dominates with 38.3% of the market, bolstered by high levels of competition, a dynamic entrepreneurial ecosystem, and significant automation adoption across industries. APAC follows with 30.7%, reflecting rapid growth fueled by digital transformation initiatives, government support for smart manufacturing, and a growing technology ecosystem in countries like India and China. EMEA contributes 26%, with steady adoption driven by compliance requirements and robust financial services, while LATAM holds 5%, showcasing opportunities for untapped potential in emerging markets.

For private equity investors, the RPA market offers not only high growth but also opportunities for value creation through strategic initiatives. Investments in niche providers with deep industry expertise can drive market fragmentation and specialization, addressing the demand for tailored automation solutions. Additionally, focusing on consolidation opportunities can strengthen portfolios and generate synergies in the fragmented provider landscape. Targeting underpenetrated regions like LATAM or industries with low adoption, such as education and public sector, can further maximize returns.

Private equity firms can also support RPA providers in overcoming key challenges such as technical complexity, talent shortages, and fragmented adoption strategies. By funding training programs, promoting Centers of Excellence, and streamlining governance frameworks, PE-backed companies can enhance their competitiveness and operational efficiencies.

In conclusion, the RPA market offers a unique intersection of rapid growth, innovation potential, and strategic value creation. For private equity, it represents an ideal platform to drive digital transformation while delivering superior returns in a technology-driven economy.

Sources & References

AI Multiple Research. (2024). 50 RPA Statistics from Surveys: Market, Adoption & Future. https://research.aimultiple.com/rpa-stats/

Deloitte. (2023). 2023 Global Shared Services and Outsourcing Survey. https://www.deloitte.com/content/dam/assets-zone2/ie/en/docs/services/consulting/2023/ie-consulting-2023-global-shared-services-and-outsourcing-survey.pdf

Flobotics. (2024). RPA Reloaded: 50+ Must-See Robotic Process Automation Statistics to Know in 2024. https://flobotics.io/blog/rpa-statistics/

Fortune Business Insights. (2024). Robotic Process Automation (RPA) Market Size, Share & Industry Analysis. https://www.fortunebusinessinsights.com/robotic-process-automation-rpa-market-102042

Grand View Research. (2023). Robotic Process Automation Market Size, Share & Trends Analysis Report. https://www.grandviewresearch.com/industry-analysis/robotic-process-automation-rpa-market

Slack. (2023). State of Work. https://d34u8crftukxnk.cloudfront.net/slackpress/prod/sites/6/State-Work-Report.en-US.pdf

Statista. (2023). Spending on robotic process automation (RPA) software worldwide from 2020 to 2032. https://www.statista.com/statistics/1309384/worldwide-rpa-software-market-size/#:~:text=Robotic%20process%20automation%20market%20size%20worldwide%202020%2D2032&text=The%20robotic%20process%20automation%20(RPA,billion%20U.S.%20dollars%20by%202032

Portulans Institute. (2024). Network Readiness Index 2024. https://networkreadinessindex.org/

World Bank. (2024). Gross Capital Formation (% of GDP). https://data.worldbank.org/indicator/NE.GDI.TOTL.ZS